Whether you are a salaried professional in Lahore, a business owner in Karachi, or a student in Islamabad, understanding the difference between a debit card and a credit card can save you thousands of rupees — and help you pick the best credit cards in Pakistan for your specific needs in 2026. Pakistan's banking sector has matured rapidly, with over 50 million debit card holders and a growing credit card user base crossing 2.5 million active accounts, according to State Bank of Pakistan data.

In this comprehensive guide, we break down every difference between debit and credit cards, review the top cards available from major Pakistani banks, and help you make an informed decision. Let's dive in.

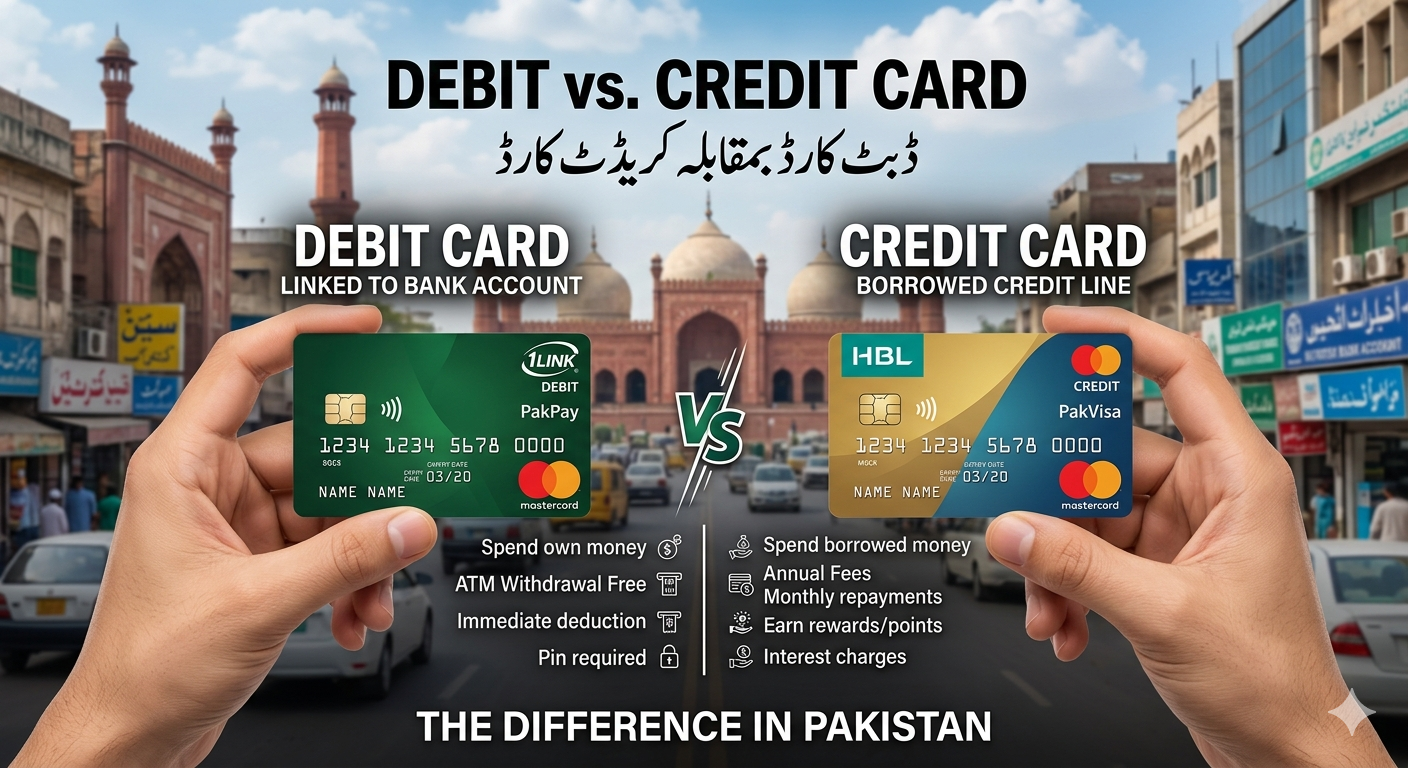

What Are Debit Cards and Credit Cards?

At the most fundamental level, a debit card is linked directly to your bank account. When you swipe it at a POS terminal or use it online, money is deducted instantly from whatever balance exists in your account. Think of it as a plastic key to your own vault — you can only spend what you already own.

A credit card, on the other hand, is a revolving line of credit extended by a bank. When you use it, you are borrowing money from the bank up to a pre-approved limit. You receive a monthly statement and can either pay the full amount (interest-free) or carry a balance (with interest/markup charges, called mark-up or profit rate in Islamic banking contexts).

In Pakistan, both card types operate on international payment networks — primarily Visa, Mastercard, and the domestically developed PayPak (NIFT-managed) network. Some premium cards also carry UnionPay branding for use in China and certain Asian markets.

If you want to build a credit history in Pakistan and enjoy purchase protection, reward points, and cashback, applying for the best credit cards in Pakistan is a smart move — provided you repay balances on time to avoid high markup rates ranging from 30%–45% APR.

Key Differences at a Glance

Here is a quick side-by-side comparison of the most important differences between debit and credit cards in the Pakistani context:

| Feature | Debit Card 🏧 | Credit Card 💳 |

|---|---|---|

| Funding Source | Your bank account balance | Bank's revolving credit line |

| Spending Limit | Your account balance | Bank-assigned credit limit |

| Interest Charges | None | 30–45% APR if balance carried |

| Reward Points | Rare / minimal | Yes — cashback, miles, points |

| Overdraft Risk | Can overdraw if enabled | No (spend up to limit) |

| Credit Score Impact | No | Yes — builds ECIB credit history |

| Fraud Liability | Higher personal risk | Lower — bank protection stronger |

| Ease of Approval | Very easy — most accounts | Requires income proof & ECIB check |

| International Use | Available (Visa/MC) | Better accepted globally |

| Annual Fee | Usually free or PKR 500–1,000 | PKR 0 – 15,000+ |

| Age Requirement | 18+ (some banks 16+) | 21+ with salary slip |

| Lounge Access | Rare | Yes (premium/platinum cards) |

| EMI Facility | No | Yes — 0% installments available |

| PayPak Network | Yes | Limited |

How Debit Cards Work in Pakistan

Pakistani banks issue debit cards automatically when you open a current or savings account. The card is linked to your IBAN and can be used at any ATM bearing the Visa, Mastercard, or PayPak logo across Pakistan's 17,000+ ATM network. Transactions are debited in real-time and you receive an SMS notification within seconds.

Types of Debit Cards in Pakistan

- PayPak Debit Card — Domestic-only card on Pakistan's NIFT network; very low or zero annual fee; available from almost all Pakistani banks including HBL, MCB, UBL, and Meezan Bank.

- Visa Debit Card — Accepted internationally; ideal for online shopping and travel.

- Mastercard Debit Card — Similar to Visa; many banks offer contactless (NFC-enabled) variants for tap-to-pay.

- UnionPay Debit Card — Issued by some banks for business travel to China and Central Asia.

Daily Transaction Limits (Typical 2026)

Pakistani banks typically impose the following limits on debit cards:

- ATM Cash Withdrawal: PKR 25,000 – 100,000 per day

- POS (Point of Sale): PKR 100,000 – 500,000 per day

- Online Transactions: PKR 50,000 – 200,000 per day (varies per bank)

How Credit Cards Work in Pakistan

Pakistani credit cards operate on a monthly billing cycle. Each time you make a purchase, the amount is deducted from your available credit. At the end of the month, you receive a statement showing the total outstanding balance and a minimum payment amount (usually 5–10% of the total balance or PKR 1,000, whichever is higher).

If you pay the full statement balance before the due date (usually 21–25 days after the statement date), no markup/interest is charged. This interest-free period is one of the biggest advantages of responsible credit card use.

If you only pay the minimum amount, Pakistani banks charge a markup rate of 3.0%–3.5% per month (36–42% annualised). Over time, this can trap cardholders in a cycle of debt. Always aim to pay the full balance each month.

How Credit Limits Are Set

Credit limits in Pakistan are determined by your monthly income, existing debt obligations (checked through State Bank's ECIB database), employment status, and the bank's internal risk scoring. A common starting limit is 2–3 months of your gross salary. Some premium cards offer limits of PKR 5,000,000 or above for high-net-worth individuals.

Best Credit Cards in Pakistan 2026

After evaluating annual fees, markup rates, reward structures, acceptance rates, and customer service quality, here are our top picks for the best credit cards in Pakistan in 2026:

- Up to 3X reward points on dining & travel

- Free airport lounge access (6 visits/year)

- Annual fee: PKR 6,500

- Credit limit up to PKR 2,000,000

- 0% EMI on top retailers

- Travel insurance included

- 4X reward points on international spend

- Cashback up to PKR 10,000/month

- Annual fee: PKR 5,000 (waivable)

- Priority Pass lounge membership

- Contactless NFC payments

- Supplementary cards available

- 100% Shariah-compliant (no riba)

- Meezan Reward Points on all purchases

- Annual fee: PKR 4,000

- Free takaful insurance cover

- Approved for halal transactions only

- No late payment interest — fixed fee structure

- Up to 5% cashback on fuel & utilities

- 3% cashback on grocery purchases

- Annual fee: PKR 3,500

- Free supplementary cards (2)

- 0% EMI on 50+ partners

- SMS alerts & UBL Digital App

- 360° Rewards on every transaction

- Exclusive dining discounts across Pakistan

- Annual fee: PKR 4,500

- Contactless & Apple Pay compatible

- Global emergency card replacement

- Online shopping protection

- Reward points redeemable for vouchers

- Balance transfer facility available

- Annual fee: PKR 2,500

- Widely accepted across Pakistan

- Easy card management via app

- Supplementary card at no extra cost

Best Debit Cards in Pakistan 2026

While this guide focuses on the best credit cards in Pakistan, debit cards remain the most popular payment instrument. Here are the standout debit cards for 2026:

| Bank | Card Name | Network | Annual Fee | Notable Feature |

|---|---|---|---|---|

| JazzCash | JazzCash Mastercard | Mastercard | Free | Mobile wallet integration, instant issuance |

| Easypaisa | Easypaisa Visa Debit | Visa | Free | RAAST transfers, QR payments |

| HBL | HBL Visa Debit Platinum | Visa | PKR 700 | HBL Pay app, NFC tap-to-pay |

| Bank Alfalah | Alfalah Mastercard Debit | Mastercard | PKR 500 | Alfalah Islami option available |

| Meezan Bank | Meezan Visa Debit | Visa | PKR 600 | Shariah-compliant, strong mobile banking |

Pros & Cons: Debit Card vs Credit Card in Pakistan

✅ Advantages of Debit Cards in Pakistan

- No debt risk — you can only spend what you have

- No annual fees on most basic PayPak and Visa debit cards

- Easy to obtain — no credit check, no salary slip required for basic accounts

- Widely used — over 50 million active debit cards across Pakistan

- Instant ATM withdrawals from a nationwide network

- Digital wallet integration — JazzCash, Easypaisa, HBL Pay

❌ Disadvantages of Debit Cards in Pakistan

- Limited fraud protection compared to credit cards

- No reward points or cashback on most cards

- No credit history building — ECIB score unaffected

- No interest-free credit period

- Lower acceptance at some international merchants

✅ Advantages of Credit Cards in Pakistan

- Reward points, cashback, and air miles accumulation

- Interest-free period of 21–25 days on full repayment

- Purchase protection and extended warranties on some premium cards

- Airport lounge access on platinum/signature cards

- 0% EMI installment plans on appliances, electronics, and medical bills

- Builds ECIB credit history for future loans and mortgages

- Emergency fund in case of unexpected expenses

❌ Disadvantages of Credit Cards in Pakistan

- High markup rate (30–45% APR) if balance is not paid in full

- Annual fees ranging from PKR 2,500 to PKR 15,000+

- Risk of overspending and debt accumulation

- Stringent eligibility criteria — requires income proof and ECIB clearance

- Hidden charges — late fees, overlimit fees, and foreign transaction fees

Which Card Should You Choose in Pakistan?

The right card depends entirely on your financial habits, income stability, and spending patterns. Here is a practical guide:

- You are new to banking or a student

- You want to avoid debt completely

- Your transactions are primarily local

- You run a small business with tight cash flow control

- You prefer mobile wallet-linked spending (JazzCash/Easypaisa)

- You have a stable monthly income (PKR 40,000+)

- You travel internationally and want lounge access + travel insurance

- You shop online frequently and want purchase protection

- You want to earn cashback or reward points on everyday spending

- You need an emergency financial buffer

- You want to build a credit history for a home loan or car financing

Security & Fraud Protection in Pakistan

Security is a major concern for Pakistani cardholders. The State Bank of Pakistan (SBP) has mandated several security enhancements including EMV chip cards (phasing out magnetic stripe), 3D Secure authentication for online transactions, and two-factor authentication via OTP for digital payments.

Credit Card vs Debit Card Fraud Liability

When a credit card is fraudulently used, SBP regulations and international network chargeback rights generally allow you to dispute the transaction and receive a refund, provided you report it within the required period (usually 45–60 days). Your own money is not directly at risk.

With a debit card, fraudulent transactions are taken directly from your bank account. While Pakistani banks have improved their fraud response, recovering debit card fraud can be more challenging and time-consuming. This makes credit cards inherently safer for online shopping.

- Never share your PIN or CVV — Pakistani banks will never ask for these over the phone

- Enable SMS alerts for every transaction

- Use virtual card numbers (available from some banks) for online shopping

- Immediately block a lost card via your bank's app or 24/7 helpline

- Regularly review your statement for unauthorized charges

Islamic Banking Cards in Pakistan

Pakistan's Islamic banking sector is one of the fastest-growing in the world, holding over 20% market share of total banking assets as of 2025. For Muslim consumers concerned about riba (interest), Islamic credit cards offer a Shariah-compliant alternative.

Islamic credit cards in Pakistan work on the Qard-e-Hasna (benevolent loan), Tawarruq, or Bai al-Inah structures depending on the bank. Instead of charging interest, banks apply a fixed fee or profit-sharing arrangement on unpaid balances.

Leading Islamic credit card providers include:

- Meezan Bank Credit Cards — Pakistan's largest Islamic bank with fully Shariah-compliant cards reviewed by a dedicated Shariah Supervisory Board

- Bank Alfalah Islami Credit Card — Available under Alfalah Islamic Banking window

- BankIslami Pakistan — Dedicated Islamic bank with Mastercard credit cards

- Dubai Islamic Bank Pakistan — International Islamic bank with strong credit card offerings

Tips to Use Cards Wisely in Pakistan (2026)

- Pay your credit card bill in full every month. The single most impactful habit. Paying the full balance before the due date means you effectively get a 21–25 day interest-free loan on every purchase.

- Use your credit card like a debit card. Only charge what you already have in your bank account. This builds credit history without accumulating debt.

- Maximise reward categories. If your card gives 3X points on dining, use it at restaurants but pay with your debit card at budget grocery stores unless the credit card also has a grocery benefit.

- Take advantage of 0% EMI offers. Buying a refrigerator, AC, or laptop? Use your credit card's 0% installment plan instead of taking a personal loan at 25%+ markup.

- Check your ECIB report annually. Your credit score (maintained by State Bank's ECIB) determines your ability to get future loans. Request your free annual credit report to ensure accuracy.

- Avoid cash advances on credit cards. Cash withdrawals via ATM on your credit card attract immediate interest (no grace period) and a cash advance fee of 2–4% — one of the most expensive forms of credit.

- Use RAAST for free bank transfers instead of cash advances — Pakistan's instant payment system allows free real-time inter-bank transfers 24/7.

- Compare annual fees vs benefits carefully. A PKR 6,000 annual fee is justified if you use lounge access worth PKR 5,000+ and earn PKR 3,000+ in cashback. Run the numbers before upgrading.

Our Verdict: Debit vs Credit Card in Pakistan 2026

Both card types serve important roles in Pakistan's evolving financial landscape. Debit cards are perfect for everyday spending control and remain the dominant payment method given Pakistan's predominantly cash-based economy still in transition to digital payments. However, for financially disciplined individuals, the best credit cards in Pakistan offer significant value — from cashback and reward points to lounge access, purchase protection, and credit history building.

If we had to choose one card for 2026, the HBL Platinum Credit Card and Meezan Bank Islamic Credit Card stand out as top all-round options, with MCB Visa Platinum closely behind for international travelers. For pure debit, JazzCash Mastercard and HBL Visa Debit lead in accessibility and features.

The bottom line: use your debit card for discipline, but unlock the real benefits of Pakistani banking with a well-chosen, responsibly-used credit card.

Frequently Asked Questions (FAQs)

A debit card deducts money directly from your savings or current account. A credit card gives you a revolving line of credit from the bank — you spend first and pay later. In Pakistan, the key practical difference is that credit cards offer interest-free periods, reward points, and purchase protection, while debit cards are simpler, debt-free instruments.

The best credit cards in Pakistan for 2026 include the HBL Platinum Credit Card (best overall), Meezan Bank Islamic Credit Card (best for Islamic banking), MCB Visa Platinum (best for international travel), UBL Cashback Card (best for everyday cashback), and Standard Chartered Titanium (best for dining rewards).

Most Pakistani banks require a minimum monthly income of PKR 40,000–50,000 for a basic credit card. Some banks like Meezan Bank and Bank Alfalah have started offering entry-level cards with a minimum salary of PKR 25,000–30,000. Premium or platinum cards typically require PKR 100,000–200,000 monthly income.

Yes, Pakistani Visa and Mastercard credit cards can be used internationally. However, foreign currency transactions attract a foreign transaction fee (typically 2–3.5%) and the currency is converted at the bank's prevailing exchange rate. State Bank of Pakistan regulations also set annual foreign currency limits for Pakistani cardholders for personal use abroad.

Conventional credit cards involve interest (riba) which is not permissible in Islam. However, Islamic credit cards from Meezan Bank, BankIslami, Bank Alfalah Islami, and Dubai Islamic Bank Pakistan are Shariah-certified and operate on riba-free structures such as Tawarruq. These are acceptable alternatives for Muslim consumers.

You can apply for a credit card in Pakistan by visiting your bank's branch, applying online through the bank's website, or via their mobile app. Required documents typically include a CNIC copy, salary slips (last 3–6 months), bank statement, and employment letter. Self-employed applicants may need to provide a business registration certificate and tax returns.

PayPak is Pakistan's first domestic payment card scheme, launched by NIFT (National Institutional Facilitation Technologies) and the State Bank of Pakistan to reduce dependence on international networks. PayPak debit cards work only within Pakistan but are nearly free to issue, making them ideal for low-income segments and financial inclusion programs.